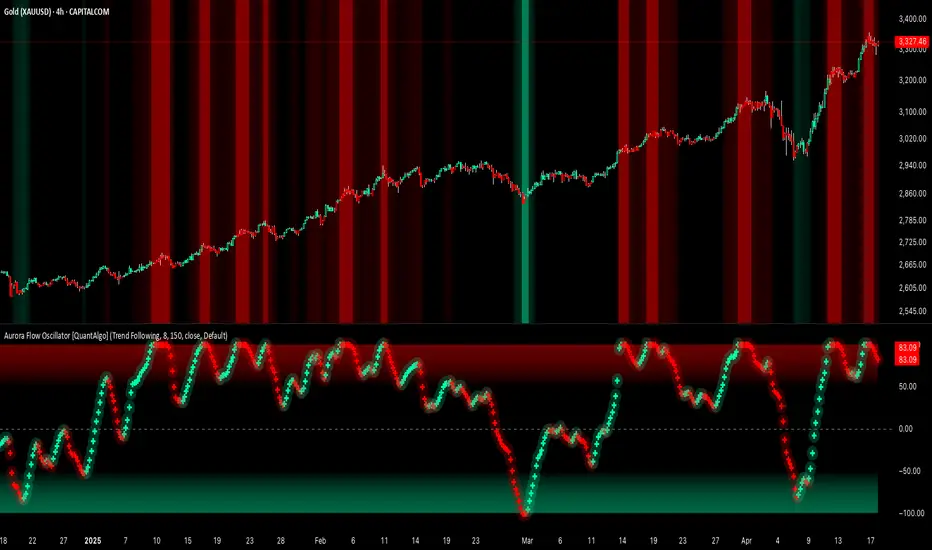

Aurora Flow Oscillator [QuantAlgo]The Aurora Flow Oscillator is an advanced momentum-based technical indicator designed to identify market direction, momentum shifts, and potential reversal zones using adaptive filtering techniques. It visualizes price momentum through a dynamic oscillator that quantifies trend strength and direction, helping traders and investors recognize momentum shifts and trading opportunities across various timeframes and asset class.

🟢 Technical Foundation

The Aurora Flow Oscillator employs a sophisticated mathematical approach with adaptive momentum filtering to analyze market conditions, including:

Price-Based Momentum Calculation: Calculates logarithmic price changes to measure the rate and magnitude of market movement

Adaptive Momentum Filtering: Applies an advanced filtering algorithm to smooth momentum calculations while preserving important signals

Acceleration Analysis: Incorporates momentum acceleration to identify shifts in market direction before they become obvious

Signal Normalization: Automatically scales the oscillator output to a range between -100 and 100 for consistent interpretation across different market conditions

The indicator processes price data through multiple filtering stages, applying mathematical principles including exponential smoothing with adaptive coefficients. This creates an oscillator that dynamically adjusts to market volatility while maintaining responsiveness to genuine trend changes.

🟢 Key Features & Signals

1. Momentum Flow and Extreme Zone Identification

The oscillator presents market momentum through an intuitive visual display that clearly indicates both direction and strength:

Above Zero: Indicates positive momentum and potential bullish conditions

Below Zero: Indicates negative momentum and potential bearish conditions

Slope Direction: The angle and direction of the oscillator provide immediate insight into momentum strength

Zero Line Crossings: Signal potential trend changes and new directional momentum

The indicator also identifies potential overbought and oversold market conditions through extreme zone markings:

Upper Zone (>50): Indicates strong bullish momentum that may be approaching exhaustion

Lower Zone (<-50): Indicates strong bearish momentum that may be approaching exhaustion

Extreme Boundaries (±95): Mark potentially unsustainable momentum levels where reversals become increasingly likely

These zones are displayed with gradient intensity that increases as the oscillator moves toward extremes, helping traders and investors:

→ Identify potential reversal zones

→ Determine appropriate entry and exit points

→ Gauge overall market sentiment strength

2. Customizable Trading Style Presets

The Aurora Flow Oscillator offers pre-configured settings for different trading approaches:

Default (80,150): Balanced configuration suitable for most trading and investing situations.

Scalping (5,80): Highly responsive settings for ultra-short-term trades. Generates frequent signals and catches quick price movements. Best for 1-15min charts when making many trades per day.

Day Trading (8,120): Optimized for intraday movements with faster response than default settings while maintaining reasonable signal quality. Ideal for 5-60min or 4h-12h timeframes.

Swing Trading (10,200): Designed for multi-day positions with stronger noise filtering. Focuses on capturing larger price swings while avoiding minor fluctuations. Works best on 1-4h and daily charts.

Position Trading (14,250): For longer-term position traders/investors seeking significant market trends. Reduces false signals by heavily filtering market noise. Ideal for daily or even weekly charts.

Trend Following (16,300): Maximum smoothing that prioritizes established directional movements over short-term fluctuations. Best used on daily and weekly charts, but can also be used for lower timeframe trading.

Countertrend (7,100): Tuned to detect potential reversals and exhaustion points in trends. More sensitive to momentum shifts than other presets. Effective on 15min-4h charts, as well as daily and weekly charts.

Each preset automatically adjusts internal parameters for optimal performance in the selected trading context, providing flexibility across different market approaches without requiring complex manual configuration.

🟢 Practical Usage Tips

1/ Trend Analysis and Interpretation

→ Direction Assessment: Evaluate the oscillator's position relative to zero to determine underlying momentum bias

→ Momentum Strength: Measure the oscillator's distance from zero within the -100 to +100 range to quantify momentum magnitude

→ Trend Consistency: Monitor the oscillator's path for sustained directional movement without frequent zero-line crossings

→ Reversal Detection: Watch for oscillator divergence from price and deceleration of movement when approaching extreme zones

2/ Signal Generation Strategies

Depending on your trading approach, multiple signal strategies can be employed:

Trend Following Signals:

Enter long positions when the oscillator crosses above zero

Enter short positions when the oscillator crosses below zero

Add to positions on pullbacks while maintaining the overall trend direction

Countertrend Signals:

Look for potential reversals when the oscillator reaches extreme zones (±95)

Enter contrary positions when momentum shows signs of exhaustion

Use oscillator divergence with price as additional confirmation

Momentum Shift Signals:

Enter positions when oscillator changes direction after establishing a trend

Exit positions when oscillator direction reverses against your position

Scale position size based on oscillator strength percentage

3/ Timeframe Optimization

The indicator can be effectively applied across different timeframes with these considerations:

Lower Timeframes (1-15min):

Use Scalping or Day Trading presets

Focus on quick momentum shifts and zero-line crossings

Be cautious of noise in extreme market conditions

Medium Timeframes (30min-4h):

Use Default or Swing Trading presets

Look for established trends and potential reversal zones

Combine with support/resistance analysis for entry/exit precision

Higher Timeframes (Daily+):

Use Position Trading or Trend Following presets

Focus on major trend identification and long-term positioning

Use extreme zones for position management rather than immediate reversals

🟢 Pro Tips

Price Momentum Period:

→ Lower values (5-7) increase sensitivity to minor price fluctuations but capture more market noise

→ Higher values (10-16) emphasize sustained momentum shifts at the cost of delayed response

→ Adjust based on your timeframe (lower for shorter timeframes, higher for longer timeframes)

Oscillator Filter Period:

→ Lower values (80-120) produce more frequent directional changes and earlier response to momentum shifts

→ Higher values (200-300) filter out shorter-term fluctuations to highlight dominant market cycles

→ Match to your typical holding period (shorter holding time = lower filter values)

Multi-Timeframe Analysis:

→ Compare oscillator readings across different timeframes for confluence

→ Look for alignment between higher and lower timeframe signals

→ Use higher timeframe for trend direction, lower for earlier entries

Volatility-Adaptive Trading:

→ Use oscillator strength to adjust position sizing (stronger = larger)

→ Consider reducing exposure when oscillator reaches extreme zones

→ Implement tighter stops during periods of oscillator acceleration

Combination Strategies:

→ Pair with volume indicators for confirmation of momentum shifts

→ Use with support/resistance levels for strategic entry and exit points

→ Combine with volatility indicators for comprehensive market context

Meanreversion

Advanced Momentum Scanner [QuantAlgo]The Advanced Momentum Scanner is a sophisticated technical indicator designed to identify market momentum and trend direction using multiple exponential moving averages (EMAs), momentum metrics, and adaptive visualization techniques. It is particularly valuable for those looking to identify trading and investing opportunities based on trend changes and momentum shifts across any market and timeframe.

🟢 Technical Foundation

The Advanced Momentum Scanner utilizes a multi-layered approach with four different EMA periods to identify market momentum and trend direction:

Ultra-Fast EMA for quick trend changes detection (default: 5)

Fast EMA for short-term trend analysis (default: 10)

Mid EMA for intermediate confirmation (default: 30)

Slow EMA for long-term trend identification (default: 100)

For momentum detection, the indicator implements a Rate of Change (RoC) calculation to measure price momentum over a specified period. It further enhances analysis by incorporating RSI readings for overbought/oversold conditions, volatility measurements through ATR, and optional volume confirmation. When these elements align, the indicator generates trading signals based on the selected sensitivity mode (Conservative, Balanced, or Aggressive).

🟢 Key Features & Signals

1. Multi-Period Trend Identification

The indicator combines multiple EMAs of different lengths to provide comprehensive trend analysis within the same timeframe, displaying the information through color-coded visual elements on the chart.

When an uptrend is detected, chart elements are colored with the bullish theme color (default: green/teal).

Similarly, when a downtrend is detected, chart elements are colored with the bearish theme color (default: red).

During neutral or indecisive periods, chart elements are colored with a neutral gray color, providing clear visual distinction between trending and non-trending market conditions.

This visualization provides immediate insights into underlying trend direction without requiring separate indicators, helping traders and investors quickly identify the market's current state.

2. Trend Strength Information Panel

The trend panel operates in three different sensitivity modes (Conservative, Aggressive, and Balanced), each affecting how the indicator processes and displays market information.

The Conservative mode prioritizes trend sustainability over frequency, showing only strong trend movements with high probability.

The Aggressive mode detects early trend changes, providing more frequent signals but potentially more false positives.

The Balanced mode offers a middle ground with moderate signal frequency and reliability.

Regardless of the selected mode, the panel displays:

Current trend direction (UPTREND, DOWNTREND, or NEUTRAL)

Trend strength percentage (0-100%)

Early detection signals when applicable

The active sensitivity mode

This comprehensive approach helps traders and investors:

→ Assess the strength of current market trends

→ Identify early potential trend changes before full confirmation

→ Make more informed trading and investing decisions based on trend context

3. Customizable Visualization Settings

This indicator offers extensive visual customization options to suit different trading styles and preferences:

Display options:

→ Fully customizable uptrend, downtrend, and neutral colors

→ Color-coded price bars showing trend direction

→ Dynamic gradient bands visualizing potential trend channels

→ Optional background coloring based on trend intensity

→ Adjustable transparency levels for all visual elements

These visualization settings can be fine-tuned through the indicator's interface, allowing traders and investors to create a personalized chart environment that emphasizes the most relevant information for their strategy.

The indicator also features a comprehensive alert system with notifications for:

New trend formations (uptrend, downtrend, neutral)

Early trend change signals

Momentum threshold crossovers

Other significant market conditions

Alerts can be customized and delivered through TradingView's notification system, making it easy to stay informed of important market developments even when you are away from the charts.

🟢 Practical Usage Tips

→ Trend Analysis and Interpretation: The indicator visualizes trend direction and strength directly on the chart through color-coding and the information panel, allowing traders and investors to immediately identify the current market context. This information helps in assessing the potential for continuation or reversal.

→ Signal Generation Strategies: The indicator generates potential trading signals based on trend direction, momentum confirmation, and selected sensitivity mode. Users can choose between Conservative (fewer but more reliable signals), Balanced (moderate approach), or Aggressive (more frequent but potentially less reliable signals).

→ Multi-Period Trend Assessment: Through its layered EMA approach, the indicator enables users to understand trend conditions across different lookback periods within the same timeframe. This helps in identifying the dominant trend and potential turning points.

🟢 Pro Tips

Adjust EMA periods based on your timeframe:

→ Lower values for shorter timeframes and more frequent signals

→ Higher values for higher timeframes and more reliable signals

Fine-tune sensitivity mode based on your trading style:

→ "Conservative" for position trading/long-term investing and fewer false signals

→ "Balanced" for swing trading/medium-term investing with moderate signal frequency

→ "Aggressive" for scalping/day trading and catching early trend changes

Look for confluence between components:

→ Strong trend strength percentage and direction in the information panel

→ Overall market context aligning with the expected direction

Use for multiple trading approaches:

→ Trend following during strong momentum periods

→ Counter-trend trading at band extremes during overextension

→ Early trend change detection with sensitivity adjustments

→ Stop loss placement using dynamic bands

Combine with:

→ Volume indicators for additional confirmation

→ Support/resistance analysis for strategic entry/exit points

→ Multiple timeframe analysis for broader market context

Gradient Range [BigBeluga]

This indicator highlights range-bound market conditions by dynamically plotting gradient-colored candlesticks within a defined price box. It detects whether the market is ranging or trending using ADX and can identify mean reversion points when price steps outside the established range.

🔵KEY FEATURES:

Range Detection Box:

➣ A transparent box is drawn based on the highest and lowest price close over a user-defined period.

➣ Helps visualize range boundaries and the midline for support/resistance reference.

Gradient Candlestick Coloring:

➣ Candles inside the range are colored with a gradient from top to bottom based on proximity to the midline.

➣ Top range candles are shaded with bearish tones, while bottom range candles use bullish tones.

Ranging/Trending State Detection:

➣ Uses ADX to determine if the market is currently in a ranging or trending state.

➣ A label in the bottom right corner shows a real-time status (🟢 Ranging / 🟡 Trending).

Mean Reversion Signal Circles:

➣ When the market is ranging, white circles are plotted at highs/lows that breach the box boundary, indicating potential mean reversion points.

➣ These levels can act as fade trade setups or exhaustion markers.

🔵USAGE:

Range Trading: Trade between the upper and lower boundaries during range-bound conditions with clearer visual feedback.

Mean Reversion Plays: Use circle signals as early alerts to identify when price extends beyond the range and may revert to the mean.

Visual Trend Strength: Instantly recognize where price is concentrated inside the range via the color gradient system.

Ranging Filter: Use the ADX label to avoid false setups during strong trending periods.

Gradient Range provides an elegant and data-driven approach to range-bound market analysis. With its gradient visualization and smart reversion detection, it empowers traders to better time entries and exits within consolidation zones.

Trend Targets [AlgoAlpha]OVERVIEW

This script combines a smoothed trend-following model with dynamic price rejection logic and ATR-based target projection to give traders a complete visual framework for trading trend continuations. It overlays on price and automatically detects potential trend shifts, confirms rejections near dynamic support/resistance, and displays calculated stop-loss and take-profit levels to support structured risk-reward management. Unlike traditional indicators that only show trend direction or signal entries, this tool brings together a unique mix of signal validation, volatility-aware positioning, and layered profit-taking to guide decision-making with more context.

CONCEPTS

The core trend logic is built on a custom Supertrend that uses an ATR-based band structure with long smoothing chains—first through a WMA, then an EMA—allowing the trend line to respond to major shifts while ignoring noise. A key addition is the use of rejection logic: the script looks for consolidation candles that "hug" the smoothed trend line and counts how many consecutive bars reject from it. This behavior often precedes significant moves. A user-defined threshold filters out weak tests and highlights only meaningful rejections.

FEATURES

Trend Detection : Automatically identifies trend direction using a smoothed Supertrend (WMA + EMA), with shape markers on trend shifts and color-coded bars for clarity.

Rejection Signals : Detects price rejections at the trend line after a user-defined number of consolidation bars; plots ▲/▼ icons to highlight strong continuation setups.

Target Projection : On trend confirmation, plots entry, stop-loss (ATR-based), and three dynamic take-profit levels based on customizable multiples.

Dynamic Updates : All levels (entry, SL, TP1–TP3) auto-adjust based on volatility and are labeled in real time on the chart.

Customization : Users can tweak trend parameters, rejection confirmation count, SL/TP ratios, smoothing lengths, and appearance settings.

Alerts : Built-in alerts for trend changes, rejection events, and when TP1, TP2, or TP3 are reached.

Chart Overlay : Plots directly on price chart with minimal clutter and clearly labeled levels for easy trading.

USAGE

Start by tuning the Supertrend factor and ATR period to fit your asset and timeframe—higher values will catch bigger swings, lower values catch faster moves. The confirmation count should match how tightly you want to filter rejection behavior—higher values make signals rarer but stronger. When the trend shifts, the indicator colors the bars and line accordingly, and if enabled, plots the full entry-TP-SL structure. Rejection markers appear only after enough qualifying bars confirm price pressure at the trend line. This is especially useful for continuation plays where price retests the trend but fails to break it. All calculations are based on volatility (ATR), so targets naturally adjust with market conditions. Add alerts to get notified of important signals even when away from the chart.

Institutional Quantum Momentum Impulse [BullByte]## Overview

The Institutional Quantum Momentum Impulse (IQMI) is a sophisticated momentum oscillator designed to detect institutional-level trend strength, volatility conditions, and market regime shifts. It combines multiple advanced technical concepts, including:

- Quantum Momentum Engine (Hilbert Transform + MACD Divergence + Stochastic Energy)

- Fractal Volatility Scoring (GARCH + Keltner-based volatility)

- Dynamic Adaptive Bands (Self-adjusting thresholds based on efficiency)

- Market Phase Detection (Volume + Momentum alignment)

- Liquidity & Cumulative Delta Analysis

The indicator provides a Z-score normalized momentum reading, making it ideal for mean-reversion and trend-following strategies.

---

## Key Features

### 1. Quantum Momentum Core

- Combines Hilbert Transform, MACD divergence, and Stochastic Energy into a single composite momentum score.

- Normalized using a Z-score for statistical significance.

- Smoothed with EMA/WMA/HMA for cleaner signals.

### 2. Dynamic Adaptive Bands

- Upper/Lower bands adjust based on volatility and efficiency ratio .

- Acts as overbought/oversold zones when momentum reaches extremes.

### 3. Market Phase Detection

- Identifies bullish , bearish , or neutral phases using:

- Volume-Weighted MA alignment

- Fractal momentum extremes

### 4. Volatility & Liquidity Filters

- Fractal Volatility Score (0-100 scale) shows market instability.

- Liquidity Check ensures trades are taken in favorable spread conditions.

### 5. Dashboard & Visuals

- Real-time dashboard with key metrics:

- Momentum strength, volatility, efficiency, cumulative delta, and market regime.

- Gradient coloring for intuitive momentum visualization .

---

## Best Trade Setups

### 1. Trend-Following Entries

- Signal :

- QM crosses above zero + Market Phase = Bullish + ADX > 25

- Cumulative Delta rising (buying pressure)

- Confirmation :

- Efficiency > 0.5 (strong momentum quality)

- Liquidity = High (tight spreads)

### 2. Mean-Reversion Entries

- Signal :

- QM touches upper band + Volatility expanding

- Market Regime = Ranging (ADX < 25)

- Confirmation :

- Efficiency < 0.3 (weak momentum follow-through)

- Cumulative Delta divergence (price high but delta declining)

### 3. Breakout Confirmation

- Signal :

- QM holds above zero after a pullback

- Market Phase shifts to Bullish/Bearish

- Confirmation :

- Volatility rising (expansion phase)

- Liquidity remains high

---

## Recommended Timeframes

- Intraday (5M - 1H): Works well for scalping & swing trades.

- Swing Trading (4H - Daily): Best for trend-following setups.

- Position Trading (Weekly+): Useful for macro trend confirmation.

---

## Input Customization

- Resonance Factor (1.0 - 3.618 ): Adjusts MACD divergence sensitivity.

- Entropy Filter (0.382/0.50/0.618) : Controls stochastic damping.

- Smoothing Type (EMA/WMA/HMA) : Changes momentum responsiveness.

- Normalization Period : Adjusts Z-score lookback.

---

The IQMI is a professional-grade momentum indicator that combines institutional-level concepts into a single, easy-to-read oscillator. It works across all markets (stocks, forex, crypto) and is ideal for traders who want:

✅ Early trend detection

✅ Volatility-adjusted signals

✅ Institutional liquidity insights

✅ Clear dashboard for quick analysis

Try it on TradingView and enhance your trading edge! 🚀

Happy Trading!

- BullByte

HEMA Trend Levels [AlgoAlpha]OVERVIEW

This script plots two Hull-EMA (HEMA) curves to define a color-coded dynamic trend zone and generate context-aware breakout levels, allowing traders to easily visualize prevailing momentum and identify high-probability breakout retests. The script blends smoothed price tracking with conditional box plotting, delivering both trend-following and mean-reversion signals within one system. It is designed to be simple to read visually while offering nuanced trend shifts and test confirmations.

█ CONCEPTS

The Hull-EMA (HEMA) is a hybrid moving average combining the responsiveness of short EMAs with the smoothness of longer ones. It applies layered smoothing: first by subtracting a full EMA from a half-length EMA (doubling the short EMA's weight), and then by smoothing the result again with the square root of the original length. This process reduces lag while maintaining clarity in direction changes. In this script, two HEMAs—fast and slow—are used to define the trend structure and trigger events when they cross. These crossovers generate "trend shift boxes"—temporary support or resistance zones drawn immediately after trend transitions—to detect price retests in the new direction. When price cleanly retests these levels, the script marks them as confirmations with triangle symbols, helping traders isolate better continuation setups. Color-coded bars further enhance visual interpretation: bullish bars when price is above both HEMAs, bearish when below, and neutral (gray) when indecisive.

█ FEATURES

Bullish and bearish bar coloring based on price and HEMA alignment.

Box plotting at each crossover (bullish or bearish) to create short-term decision zones.

Real-time test detection: price must cleanly test and bounce from box levels to be considered valid.

Multiple alert conditions: crossover alerts, test alerts, and trend continuation alerts.

█ USAGE

Use this indicator on any time frame and asset. Adjust HEMA lengths to match your trading style—shorter lengths for scalping or intraday, longer for swing trading. The shaded area between HEMAs helps visually define the current trend. Watch for crossovers: a bullish crossover plots a green support box just below price, and a bearish one plots a red resistance box just above. These zones act as short-term decision points. When price returns to test a box and confirms with strong rejection (e.g., closes above for bullish or below for bearish), a triangle symbol is plotted. These tests can signal strong trend continuation. For traders looking for clean entries, combining the crossover with a successful retest improves reliability. Alerts can be enabled for all key signals: trend shift, test confirmations, and continuation conditions, making it suitable for automated setups or discretionary traders tracking multiple charts.

Multi-Anchored Linear Regression Channels [TANHEF]█ Overview:

The 'Multi-Anchored Linear Regression Channels ' plots multiple dynamic regression channels (or bands) with unique selectable calculation types for both regression and deviation. It leverages a variety of techniques, customizable anchor sources to determine regression lengths, and user-defined criteria to highlight potential opportunities.

Before getting started, it's worth exploring all sections, but make sure to review the Setup & Configuration section in particular. It covers key parameters like anchor type, regression length, bias, and signal criteria—essential for aligning the tool with your trading strategy.

█ Key Features:

⯁ Multi-Regression Capability:

Plot up to three distinct regression channels and/or bands simultaneously, each with customizable anchor types to define their length.

⯁ Regression & Deviation Methods:

Regressions Types:

Standard: Uses ordinary least squares to compute a simple linear trend by averaging the data and deriving a slope and endpoints over the lookback period.

Ridge: Introduces L2 regularization to stabilize the slope by penalizing large coefficients, which helps mitigate multicollinearity in the data.

Lasso: Uses L1 regularization through soft-thresholding to shrink less important coefficients, yielding a simpler model that highlights key trends.

Elastic Net: Combines L1 and L2 penalties to balance coefficient shrinkage and selection, producing a robust weighted slope that handles redundant predictors.

Huber: Implements the Huber loss with iteratively reweighted least squares (IRLS) and EMA-style weights to reduce the impact of outliers while estimating the slope.

Least Absolute Deviations (LAD): Reduces absolute errors using iteratively reweighted least squares (IRLS), yielding a slope less sensitive to outliers than squared-error methods.

Bayesian Linear: Merges prior beliefs with weighted data through Bayesian updating, balancing the prior slope with data evidence to derive a probabilistic trend.

Deviation Types:

Regressive Linear (Reverse): In reverse order (recent to oldest), compute weighted squared differences between the data and a line defined by a starting value and slope.

Progressive Linear (Forward): In forward order (oldest to recent), compute weighted squared differences between the data and a line defined by a starting value and slope.

Balanced Linear: In forward order (oldest to newest), compute regression, then pair to source data in reverse order (newest to oldest) to compute weighted squared differences.

Mean Absolute: Compute weighted absolute differences between each data point and its regression line value, then aggregate them to yield an average deviation.

Median Absolute: Determine the weighted median of the absolute differences between each data point and its regression line value to capture the central tendency of deviations.

Percent: Compute deviation as a percentage of a base value by multiplying that base by the specified percentage, yielding symmetric positive and negative deviations.

Fitted: Compare a regression line with high and low series values by computing weighted differences to determine the maximum upward and downward deviations.

Average True Range: Iteratively compute the weighted average of absolute differences between the data and its regression line to yield an ATR-style deviation measure.

Bias:

Bias: Applies EMA or inverse-EMA style weighting to both Regression and/or Deviation, emphasizing either recent or older data.

⯁ Customizable Regression Length via Anchors:

Anchor Types:

Fixed: Length.

Bar-Based: Bar Highest/Lowest, Volume Highest/Lowest, Spread Highest/Lowest.

Correlation: R Zero, R Highest, R Lowest, R Absolute.

Slope: Slope Zero, Slope Highest, Slope Lowest, Slope Absolute.

Indicator-Based: Indicators Highest/Lowest (ADX, ATR, BBW, CCI, MACD, RSI, Stoch).

Time-Based: Time (Day, Week, Month, Quarter, Year, Decade, Custom).

Session-Based: Session (Tokyo, London, New York, Sydney, Custom).

Event-Based: Earnings, Dividends, Splits.

External: Input Source Highest/Lowest.

Length Selection:

Maximum: The highest allowed regression length (also fixed value of “Length” anchor).

Minimum: The shortest allowed length, ensuring enough bars for a valid regression.

Step: The sampling interval (e.g., 1 checks every bar, 2 checks every other bar, etc.). Increasing the step reduces the loading time, most applicable to “Slope” and “R” anchors.

Adaptive lookback:

Adaptive Lookback: Enable to display regression regardless of too few historical bars.

⯁ Selecting Bias:

Bias applies separately to regression and deviation.

Positive values emphasize recent data (EMA-style), negative invert, and near-zero maintains balance. (e.g., a length 100, bias +1 gives the newest price ~7× more weight than the oldest).

It's best to apply bias to both (regression and deviation) or just the deviation. Biasing only regression may distort deviation visually, while biasing both keeps their relationship intuitive. Using bias only for deviation scales it without altering regression, offering unique analysis.

⯁ Scale Awareness:

Supports linear and logarithmic price scaling, the regression and deviations adjust accordingly.

⯁ Signal Generation & Alerts:

Customizable entry/exit signals and alerts, detailed in the dedicated section below.

⯁ Visual Enhancements & Real-World Examples:

Optional on-chart table display summarizing regression input criteria (display type, anchor type, source, regression type, regression bias, deviation type, deviation bias, deviation multiplier) and key calculated metrics (regression length, slope, Pearson’s R, percentage position within deviations, etc.) for quick reference.

█ Understanding R (Pearson Correlation Coefficient):

Pearson’s R gauges data alignment to a straight-line trend within the regression length:

Range: R varies between –1 and +1.

R = +1 → Perfect positive correlation (strong uptrend).

R = 0 → No linear relationship detected.

R = –1 → Perfect negative correlation (strong downtrend).

This script uses Pearson’s R as an anchor, adjusting regression length to target specific R traits. Strong R (±1) follows the regression channel, while weak R (0) shows inconsistency.

█ Understanding the Slope:

The slope is the direction and rate at which the regression line rises or falls per bar:

Positive Slope (>0): Uptrend – Steeper means faster increase.

Negative Slope (<0): Downtrend – Steeper means sharper drop.

Zero or Near-Zero Slope: Sideways – Indicating range-bound conditions.

This script uses highest and lowest slope as an anchor, where extremes highlight strong moves and trend lines, while values near zero indicate sideways action and possible support/resistance.

█ Setup & Configuration:

Whether you’re new to this script or want to quickly adjust all critical parameters, the panel below shows the main settings available. You can customize everything from the anchor type and maximum length to the bias, signal conditions, and more.

Scale (select Log Scale for logarithmic, otherwise linear scale).

Display (regression channel and/or bands).

Anchor (how regression length is determined).

Length (control bars analyzed):

• Max – Upper limit.

• Min – Prevents regression from becoming too short.

• Step – Controls scanning precision; increasing Step reduces load time.

Regression:

• Type – Calculation method.

• Bias – EMA-style emphasis (>0=new bars weighted more; <0=old bars weighted more).

Deviation:

• Type – Calculation method.

• Bias – EMA-style emphasis (>0=new bars weighted more; <0=old bars weighted more).

• Multiplier - Adjusts Upper and Lower Deviation.

Signal Criteria:

• % (Price vs Deviation) – (0% = lower deviation, 50% = regression, 100% = upper deviation).

• R – (0 = no correlation, ±1 = perfect correlation; >0 = +slope, <0 = -slope).

Table (analyze table of input settings, calculated results, and signal criteria).

Adaptive Lookback (display regression while too few historical bars).

Multiple Regressions (steps 2 to 7 apply to #1, #2, and #3 regressions).

█ Signal Generation & Alerts:

The script offers customizable entry and exit signals with flexible criteria and visual cues (background color, dots, or triangles). Alerts can also be triggered for these opportunities.

Percent Direction Criteria:

(0% = lower deviation, 50% = regression line, 100% = upper deviation)

Above %: Triggers if price is above a specified percent of the deviation channel.

Below %: Triggers if price is below a specified percent of the deviation channel.

(Blank): Ignores the percent‐based condition.

Pearson's R (Correlation) Direction Criteria:

(0 = no correlation, ±1 = perfect correlation; >0 = positive slope, <0 = negative slope)

Above R / Below R: Compares the correlation to a threshold.

Above│R│ / Below│R│: Uses absolute correlation to focus on strength, ignoring direction.

Zero to R: Checks if R is in the 0-to-threshold range.

(Blank): Ignores correlation-based conditions.

█ User Tips & Best Practices:

Choose an anchor type that suits your strategy, “Bar Highest/Lowest” automatically spots commonly used regression zones, while “│R│ Highest” targets strong linear trends.

Consider enabling or disabling the Adaptive Lookback feature to ensure you always have a plotted regression if your chart doesn’t meet the maximum-length requirement.

Use a small Step size (1) unless relying on R-correlation or slope-based anchors as the are time-consuming to calculate. Larger steps speed up calculations but reduce precision.

Fine-tune settings such as lookback periods, regression bias, and deviation multipliers, or trend strength. Small adjustments can significantly affect how channels and signals behave.

To reduce loading time , show only channels (not bands) and disable signals, this limits calculations to the last bar and supports more extreme criteria.

Use the table display to monitor anchor type, calculated length, slope, R value, and percent location at a glance—especially if you have multiple regressions visible simultaneously.

█ Conclusion:

With its blend of advanced regression techniques, flexible deviation options, and a wide range of anchor types, this indicator offers a highly adaptable linear regression channeling system. Whether you're anchoring to time, price extremes, correlation, slope, or external events, the tool can be shaped to fit a variety of strategies. Combined with customizable signals and alerts, it may help highlight areas of confluence and support a more structured approach to identifying potential opportunities.

LinearRegressionLibrary "LinearRegression"

Calculates a variety of linear regression and deviation types, with optional emphasis weighting. Additionally, multiple of slope and Pearson’s R calculations.

calcSlope(_src, _len, _condition)

Calculates the slope of a linear regression over the specified length.

Parameters:

_src (float) : (float) The source data.

_len (int) : (int) The length of the lookback period for the linear regression.

_condition (bool) : (bool) Flag to enable calculation. Set to true to calculate on every bar; otherwise, set to barstate.islast for efficiency.

Returns: (float) The slope of the linear regression.

calcReg(_src, _len, _condition)

Calculates a basic linear regression, returning y1, y2, slope, and average.

Parameters:

_src (float) : (float) The source data series.

_len (int) : (int) The length of the lookback period.

_condition (bool) : (bool) Flag to enable calculation (true = calculate).

Returns: (float ) An array of 4 values: .

calcRegStandard(_src, _len, _emphasis, _condition)

Calculates an Standard linear regression with optional emphasis.

Parameters:

_src (float) : (series float) The source data series.

_len (int) : (int) The length of the lookback period.

_emphasis (float) : (float) The emphasis factor: 0 for equal weight; >0 emphasizes recent bars; <0 emphasizes older bars.

_condition (bool) : (bool) Flag to enable calculation (true = calculate).

Returns: (float ) .

calcRegRidge(_src, _len, lambda, _emphasis, _condition)

Calculates a ridge regression with optional emphasis.

Parameters:

_src (float) : (float) The source data series.

_len (int) : (int) The length of the lookback period.

lambda (float) : (float) The ridge regularization parameter.

_emphasis (float) : (float) The emphasis factor: 0 for equal weight; >0 emphasizes recent bars; <0 emphasizes older bars.

_condition (bool) : (bool) Flag to enable calculation (true = calculate).

Returns: (float ) .

calcRegLasso(_src, _len, lambda, _emphasis, _condition)

Calculates a Lasso regression with optional emphasis.

Parameters:

_src (float) : (float) The source data series.

_len (int) : (int) The length of the lookback period.

lambda (float) : (float) The Lasso regularization parameter.

_emphasis (float) : (float) The emphasis factor: 0 for equal weight; >0 emphasizes recent bars; <0 emphasizes older bars.

_condition (bool) : (bool) Flag to enable calculation (true = calculate).

Returns: (float ) .

calcElasticNetLinReg(_src, _len, lambda1, lambda2, _emphasis, _condition)

Calculates an Elastic Net regression with optional emphasis.

Parameters:

_src (float) : (float) The source data series.

_len (int) : (int) The length of the lookback period.

lambda1 (float) : (float) L1 regularization parameter (Lasso).

lambda2 (float) : (float) L2 regularization parameter (Ridge).

_emphasis (float) : (float) Emphasis factor: 0 for equal weight; >0 emphasizes recent bars; <0 emphasizes older bars.

_condition (bool) : (bool) Flag to enable calculation (true = calculate).

Returns: (float ) .

calcRegHuber(_src, _len, delta, iterations, _emphasis, _condition)

Calculates a Huber regression using Iteratively Reweighted Least Squares (IRLS).

Parameters:

_src (float) : (float) The source data series.

_len (int) : (int) The length of the lookback period.

delta (float) : (float) Huber threshold parameter.

iterations (int) : (int) Number of IRLS iterations.

_emphasis (float) : (float) Emphasis factor: 0 for equal weight; >0 emphasizes recent bars; <0 emphasizes older bars.

_condition (bool) : (bool) Flag to enable calculation (true = calculate).

Returns: (float ) .

calcRegLAD(_src, _len, iterations, _emphasis, _condition)

Calculates a Least Absolute Deviations (LAD) regression via IRLS.

Parameters:

_src (float) : (float) The source data series.

_len (int) : (int) The length of the lookback period.

iterations (int) : (int) Number of IRLS iterations for LAD.

_emphasis (float) : (float) Emphasis factor: 0 for equal weight; >0 emphasizes recent bars; <0 emphasizes older bars.

_condition (bool) : (bool) Flag to enable calculation (true = calculate).

Returns: (float ) .

calcRegBayesian(_src, _len, priorMean, priorSpan, sigma, _emphasis, _condition)

Calculates a Bayesian linear regression with optional emphasis.

Parameters:

_src (float) : (float) The source data series.

_len (int) : (int) The length of the lookback period.

priorMean (float) : (float) The prior mean for the slope.

priorSpan (float) : (float) The prior variance (or span) for the slope.

sigma (float) : (float) The assumed standard deviation of residuals.

_emphasis (float) : (float) Emphasis factor: 0 for equal weight; >0 emphasizes recent bars; <0 emphasizes older bars.

_condition (bool) : (bool) Flag to enable calculation (true = calculate).

Returns: (float ) .

calcRFromLinReg(_src, _len, _slope, _average, _y1, _condition)

Calculates the Pearson correlation coefficient (R) based on linear regression parameters.

Parameters:

_src (float) : (float) The source data.

_len (int) : (int) The length of the lookback period.

_slope (float) : (float) The slope of the linear regression.

_average (float) : (float) The average value of the source data series.

_y1 (float) : (float) The starting point (y-intercept of the oldest bar) for the linear regression.

_condition (bool) : (bool) Flag to enable calculation. Set to true to calculate on every bar; otherwise, set to barstate.islast for efficiency.

Returns: (float) The Pearson correlation coefficient (R) adjusted for the direction of the slope.

calcRFromSource(_src, _len, _condition)

Calculates the correlation coefficient (R) using a specified length and source data.

Parameters:

_src (float) : (float) The source data.

_len (int) : (int) The length of the lookback period.

_condition (bool) : (bool) Flag to enable calculation. Set to true to calculate on every bar; otherwise, set to barstate.islast for efficiency.

Returns: (float) The correlation coefficient (R).

calcSlopeLengthZero(_src, _len, _minLen, _step, _condition)

Identifies the length at which the slope is flattest (closest to zero).

Parameters:

_src (float) : (float) The source data.

_len (int) : (int) The maximum lookback length to consider (minimum of 2).

_minLen (int) : (int) The minimum length to start from (cannot exceed the max length).

_step (int) : (int) The increment step for lengths.

_condition (bool) : (bool) Flag to enable calculation. Set to true to calculate on every bar; otherwise, set to barstate.islast.

Returns: (int) The length at which the slope is flattest.

calcSlopeLengthHighest(_src, _len, _minLen, _step, _condition)

Identifies the length at which the slope is highest.

Parameters:

_src (float) : (float) The source data.

_len (int) : (int) The maximum lookback length (minimum of 2).

_minLen (int) : (int) The minimum length to start from.

_step (int) : (int) The step for incrementing lengths.

_condition (bool) : (bool) Flag to enable calculation. Set to true to calculate on every bar; otherwise, set to barstate.islast.

Returns: (int) The length at which the slope is highest.

calcSlopeLengthLowest(_src, _len, _minLen, _step, _condition)

Identifies the length at which the slope is lowest.

Parameters:

_src (float) : (float) The source data.

_len (int) : (int) The maximum lookback length (minimum of 2).

_minLen (int) : (int) The minimum length to start from.

_step (int) : (int) The step for incrementing lengths.

_condition (bool) : (bool) Flag to enable calculation. Set to true to calculate on every bar; otherwise, set to barstate.islast.

Returns: (int) The length at which the slope is lowest.

calcSlopeLengthAbsolute(_src, _len, _minLen, _step, _condition)

Identifies the length at which the absolute slope value is highest.

Parameters:

_src (float) : (float) The source data.

_len (int) : (int) The maximum lookback length (minimum of 2).

_minLen (int) : (int) The minimum length to start from.

_step (int) : (int) The step for incrementing lengths.

_condition (bool) : (bool) Flag to enable calculation. Set to true to calculate on every bar; otherwise, set to barstate.islast.

Returns: (int) The length at which the absolute slope value is highest.

calcRLengthZero(_src, _len, _minLen, _step, _condition)

Identifies the length with the lowest absolute R value.

Parameters:

_src (float) : (float) The source data.

_len (int) : (int) The maximum lookback length (minimum of 2).

_minLen (int) : (int) The minimum length to start from.

_step (int) : (int) The step for incrementing lengths.

_condition (bool) : (bool) Flag to enable calculation. Set to true to calculate on every bar; otherwise, set to barstate.islast.

Returns: (int) The length with the lowest absolute R value.

calcRLengthHighest(_src, _len, _minLen, _step, _condition)

Identifies the length with the highest R value.

Parameters:

_src (float) : (float) The source data.

_len (int) : (int) The maximum lookback length (minimum of 2).

_minLen (int) : (int) The minimum length to start from.

_step (int) : (int) The step for incrementing lengths.

_condition (bool) : (bool) Flag to enable calculation. Set to true to calculate on every bar; otherwise, set to barstate.islast.

Returns: (int) The length with the highest R value.

calcRLengthLowest(_src, _len, _minLen, _step, _condition)

Identifies the length with the lowest R value.

Parameters:

_src (float) : (float) The source data.

_len (int) : (int) The maximum lookback length (minimum of 2).

_minLen (int) : (int) The minimum length to start from.

_step (int) : (int) The step for incrementing lengths.

_condition (bool) : (bool) Flag to enable calculation. Set to true to calculate on every bar; otherwise, set to barstate.islast.

Returns: (int) The length with the lowest R value.

calcRLengthAbsolute(_src, _len, _minLen, _step, _condition)

Identifies the length with the highest absolute R value.

Parameters:

_src (float) : (float) The source data.

_len (int) : (int) The maximum lookback length (minimum of 2).

_minLen (int) : (int) The minimum length to start from.

_step (int) : (int) The step for incrementing lengths.

_condition (bool) : (bool) Flag to enable calculation. Set to true to calculate on every bar; otherwise, set to barstate.islast.

Returns: (int) The length with the highest absolute R value.

calcDevReverse(_src, _len, _slope, _y1, _inputDev, _emphasis, _condition)

Calculates the regressive linear deviation in reverse order, with optional emphasis on recent data.

Parameters:

_src (float) : (float) The source data.

_len (int) : (int) The length of the lookback period.

_slope (float) : (float) The slope of the linear regression.

_y1 (float) : (float) The y-intercept (oldest bar) of the linear regression.

_inputDev (float) : (float) The input deviation multiplier.

_emphasis (float) : (float) Emphasis factor: 0 for equal weight; >0 emphasizes recent bars; <0 emphasizes older bars.

_condition (bool) : (bool) Flag to enable calculation (true = calculate).

Returns: A 2-element tuple: .

calcDevForward(_src, _len, _slope, _y1, _inputDev, _emphasis, _condition)

Calculates the progressive linear deviation in forward order (oldest to most recent bar), with optional emphasis.

Parameters:

_src (float) : (float) The source data array, where _src is oldest and _src is most recent.

_len (int) : (int) The length of the lookback period.

_slope (float) : (float) The slope of the linear regression.

_y1 (float) : (float) The y-intercept of the linear regression (value at the most recent bar, adjusted by slope).

_inputDev (float) : (float) The input deviation multiplier.

_emphasis (float) : (float) Emphasis factor: 0 for equal weight; >0 emphasizes recent bars; <0 emphasizes older bars.

_condition (bool) : (bool) Flag to enable calculation (true = calculate).

Returns: A 2-element tuple: .

calcDevBalanced(_src, _len, _slope, _y1, _inputDev, _emphasis, _condition)

Calculates the balanced linear deviation with optional emphasis on recent or older data.

Parameters:

_src (float) : (float) Source data array, where _src is the most recent and _src is the oldest.

_len (int) : (int) The length of the lookback period.

_slope (float) : (float) The slope of the linear regression.

_y1 (float) : (float) The y-intercept of the linear regression (value at the oldest bar).

_inputDev (float) : (float) The input deviation multiplier.

_emphasis (float) : (float) Emphasis factor: 0 for equal weight; >0 emphasizes recent bars; <0 emphasizes older bars.

_condition (bool) : (bool) Flag to enable calculation (true = calculate).

Returns: A 2-element tuple: .

calcDevMean(_src, _len, _slope, _y1, _inputDev, _emphasis, _condition)

Calculates the mean absolute deviation from a forward-applied linear trend (oldest to most recent), with optional emphasis.

Parameters:

_src (float) : (float) The source data array, where _src is the most recent and _src is the oldest.

_len (int) : (int) The length of the lookback period.

_slope (float) : (float) The slope of the linear regression.

_y1 (float) : (float) The y-intercept (oldest bar) of the linear regression.

_inputDev (float) : (float) The input deviation multiplier.

_emphasis (float) : (float) Emphasis factor: 0 for equal weight; >0 emphasizes recent bars; <0 emphasizes older bars.

_condition (bool) : (bool) Flag to enable calculation (true = calculate).

Returns: A 2-element tuple: .

calcDevMedian(_src, _len, _slope, _y1, _inputDev, _emphasis, _condition)

Calculates the median absolute deviation with optional emphasis on recent data.

Parameters:

_src (float) : (float) The source data array (index 0 = oldest, index _len - 1 = most recent).

_len (int) : (int) The length of the lookback period.

_slope (float) : (float) The slope of the linear regression.

_y1 (float) : (float) The y-intercept (oldest bar) of the linear regression.

_inputDev (float) : (float) The deviation multiplier.

_emphasis (float) : (float) Emphasis factor: 0 for equal weight; >0 emphasizes recent bars; <0 emphasizes older bars.

_condition (bool) : (bool) Flag to enable calculation (true = calculate).

Returns:

calcDevPercent(_y1, _inputDev, _condition)

Calculates the percent deviation from a given value and a specified percentage.

Parameters:

_y1 (float) : (float) The base value from which to calculate deviation.

_inputDev (float) : (float) The deviation percentage.

_condition (bool) : (bool) Flag to enable calculation (true = calculate).

Returns: A 2-element tuple: .

calcDevFitted(_len, _slope, _y1, _emphasis, _condition)

Calculates the weighted fitted deviation based on high and low series data, showing max deviation, with optional emphasis.

Parameters:

_len (int) : (int) The length of the lookback period.

_slope (float) : (float) The slope of the linear regression.

_y1 (float) : (float) The Y-intercept (oldest bar) of the linear regression.

_emphasis (float) : (float) Emphasis factor: 0 for equal weight; >0 emphasizes recent bars; <0 emphasizes older bars.

_condition (bool) : (bool) Flag to enable calculation (true = calculate).

Returns: A 2-element tuple: .

calcDevATR(_src, _len, _slope, _y1, _inputDev, _emphasis, _condition)

Calculates an ATR-style deviation with optional emphasis on recent data.

Parameters:

_src (float) : (float) The source data (typically close).

_len (int) : (int) The length of the lookback period.

_slope (float) : (float) The slope of the linear regression.

_y1 (float) : (float) The Y-intercept (oldest bar) of the linear regression.

_inputDev (float) : (float) The input deviation multiplier.

_emphasis (float) : (float) Emphasis factor: 0 for equal weight; >0 emphasizes recent bars; <0 emphasizes older bars.

_condition (bool) : (bool) Flag to enable calculation (true = calculate).

Returns: A 2-element tuple: .

calcPricePositionPercent(_top, _bot, _src)

Calculates the percent position of a price within a linear regression channel. Top=100%, Bottom=0%.

Parameters:

_top (float) : (float) The top (positive) deviation, corresponding to 100%.

_bot (float) : (float) The bottom (negative) deviation, corresponding to 0%.

_src (float) : (float) The source price.

Returns: (float) The percent position within the channel.

plotLinReg(_len, _y1, _y2, _slope, _devTop, _devBot, _scaleTypeLog, _lineWidth, _extendLines, _channelStyle, _colorFill, _colUpLine, _colDnLine, _colUpFill, _colDnFill)

Plots the linear regression line and its deviations, with configurable styles and fill.

Parameters:

_len (int) : (int) The lookback period for the linear regression.

_y1 (float) : (float) The starting y-value of the regression line.

_y2 (float) : (float) The ending y-value of the regression line.

_slope (float) : (float) The slope of the regression line (used to determine line color).

_devTop (float) : (float) The top deviation to add to the line.

_devBot (float) : (float) The bottom deviation to subtract from the line.

_scaleTypeLog (bool) : (bool) Use a log scale if true; otherwise, linear scale.

_lineWidth (int) : (int) The width of the plotted lines.

_extendLines (string) : (string) How lines should extend (none, left, right, both).

_channelStyle (string) : (string) The style of the channel lines (solid, dashed, dotted).

_colorFill (bool) : (bool) Whether to fill the space between the top and bottom deviation lines.

_colUpLine (color) : (color) Line color when slope is positive.

_colDnLine (color) : (color) Line color when slope is negative.

_colUpFill (color) : (color) Fill color when slope is positive.

_colDnFill (color) : (color) Fill color when slope is negative.

Range Breakout Signals [AlgoAlpha]OVERVIEW

This script detects range-bound market conditions and breakout signals using a combination of volatility compression and volume imbalance analysis. It identifies zones where price consolidates within a defined range and highlights potential breakout points with visual markers. Traders can use this to spot market transitions from ranging to trending phases, aiding in decision-making for breakout strategies.

CONCEPTS

The script measures volatility by comparing the ratio of the simple moving average (SMA) of price movements to their median value. When volatility drops below a threshold, the script assumes a range-bound market. It then tracks the cumulative volume of buying and selling pressure to assess breakout strength. The approach is based on the idea that market consolidation often precedes strong moves, and volume distribution can provide clues on the breakout direction.

FEATURES

Range Detection : Uses a volatility filter to identify low-volatility zones and marks them on the chart with shaded boxes.

Volume Imbalance Analysis : Evaluates cumulative up and down volume over a confirmation period to assess directional bias.

Breakout Signals : When price exits a detected range, the script plots breakout markers. A ▲ symbol indicates a bullish breakout, and a ▼ symbol indicates a bearish breakout. Additional "+" markers indicate strong volume imbalance favoring the breakout direction.

Adaptive Timeframe Volume Analysis : The script dynamically adjusts its volume calculation based on the chart’s timeframe, ensuring reliable signal generation across different trading conditions.

Alerts : Notifies traders when a new range is detected or when a breakout occurs, allowing for automated monitoring.

USAGE

Traders can use this script to identify potential trade setups by entering positions when price breaks out of a detected range. For breakout confirmation, traders can look at volume imbalance cues—bullish breakouts with strong buying volume may indicate sustained moves, while weak volume breakouts may lead to false signals. This script is particularly useful for breakout traders, range traders seeking to fade breakouts, and those looking to automate trade alerts in volatile markets.

Wyckoff Event Detection [Alpha Extract]Wyckoff Event Detection

A powerful and intelligent indicator designed to detect key Wyckoff events in real time, helping traders analyze market structure and anticipate potential trend shifts. Using volume and price action, this script automatically identifies distribution and accumulation phases, providing traders with valuable insights into market behavior.

🔶 Phase-Based Detection

Utilizes a phase detection algorithm that evaluates price and volume conditions to identify accumulation (bullish) and distribution (bearish) events. This method ensures the script effectively captures major market turning points and avoids noise.

🔶 Multi-Factor Event Recognition

Incorporates multiple event conditions, including upthrusts, selling climaxes, and springs, to detect high-probability entry and exit points. Each event is filtered through customizable sensitivity settings, ensuring precise detection aligned with different trading styles.

🔶 Customizable Parameters

Fine-tune event detection with adjustable thresholds for volume, price movement, trend strength, and event spacing. These inputs allow traders to personalize the script to match their strategy and risk tolerance.

// === USER INPUTS ===

i_volLen = input.int(20, "Volume MA Length", minval=1)

i_priceLookback = input.int(20, "Price Pattern Lookback", minval=5)

i_lineLength = input.int(15, "Line Length", minval=5)

i_labelSpacing = input.int(5, "Minimum Label Spacing (bars)", minval=1, maxval=20)

❓How It Works

🔶 Event Identification

The script scans for key Wyckoff events by analyzing volume spikes, price deviations, and trend shifts within a user-defined lookback period. It categorizes events into bullish (accumulation) or bearish (distribution) structures and plots them directly on the chart.

// === EVENT DETECTION ===

volMA = ta.sma(volume, i_volLen)

highestHigh = ta.highest(high, i_priceLookback)

lowestLow = ta.lowest(low, i_priceLookback)

🔶 Automatic Filtering & Cleanup

Unconfirmed or weak signals are filtered out using customizable strength multipliers and volume thresholds. Events that do not meet the minimum conditions are discarded to keep the chart clean and informative.

🔶 Phase Strength Analysis

The script continuously tracks bullish and bearish event counts to determine whether the market is currently in an accumulation, distribution, or neutral phase. This allows traders to align their strategies accordingly.

🔶 Visual Alerts & Labels

Detects and labels key Wyckoff events directly on the chart, providing immediate insights into market conditions:

- PSY (Preliminary Supply) and UT (Upthrust) for distribution phases.

- PS (Preliminary Support) and SC (Selling Climax) for accumulation phases.

- Labels adjust dynamically to avoid chart clutter and improve readability.

🔶 Entry & Exit Optimization

By highlighting supply and demand imbalances, the script assists traders in identifying optimal entry and exit points. Wyckoff concepts such as springs and upthrusts provide clear trade signals based on market structure.

🔶 Trend Confirmation & Risk Management

Observing how price reacts to detected events helps confirm trend direction and potential reversals. Traders can place stop-loss and take-profit levels based on Wyckoff phase analysis, ensuring strategic trade execution.

🔶 Table-Based Market Analysis (Table)

A built-in table summarizes:

- Market Phase: Accumulation, Distribution, or Neutral.

- Strength of Phase: Weak, Moderate, or Strong.

- Price Positioning: Whether price is near support, resistance, or in a trading range.

- Supply/Demand State: Identifies whether the market is supply or demand dominant.

🔶 Why Choose Wyckoff Market Phases - Alpha Extract?

This indicator offers a systematic approach to understanding market mechanics through the lens of Wyckoff's time-tested principles. By providing clear and actionable insights into market phases, it empowers traders to make informed decisions, enhancing both confidence and performance in various trading environments.

Liquidity Depth [AlgoAlpha]OVERVIEW

This script visualizes market liquidity by identifying key price levels where significant volume has transacted. It highlights zones of high buying and selling interest, helping traders understand where liquidity is accumulating and how price may respond to these areas. By dynamically tracking volume at highs and lows, the script builds a real-time liquidity profile, making it a powerful tool for identifying potential support and resistance levels.

CONCEPTS

Liquidity depth analysis helps traders determine how price interacts with supply and demand at different levels. The script processes historical volume data to distinguish between high-liquidity and low-liquidity zones. It assigns transparency levels to plotted lines , ensuring that more relevant liquidity areas stand out visually. The script adds a profile to show the depth of liquidity (derived from historical volume data) for levels above and below the current price

FEATURES

Liquidity Levels: Tracks liquidity levels based on volume concentration at price high and lows.

Volume-Based Transparency: More significant liquidity levels are displayed with higher visibility, showing their significance.

Interpolation: interpolates the bullish and bearish liquidity depth at a user defined range away from the price, helping in comparing the liquidity amounts between bullish and bearish.

Depth Profile: Allows traders to visualize depth of liquidity in a more quantitative and clearer way than the liquidity levels/list]

USAGE

This indicator is best used to track liquidity levels and potential price reaction areas. Traders can adjust the Liquidity Lookback setting to analyze past liquidity levels over different historical periods. The Profile Resolution setting controls the granularity of liquidity depth visualization, with higher values providing more detail. The script can be applied across different timeframes, from intraday scalping to swing trading analysis. The plotted liquidity zones provide traders with insights into where price may encounter strong support, resistance, or potential liquidity-driven reversals.

Uptrick: Time Based ReversionIntroduction

The Uptrick: Time Based Reversion indicator is designed to provide a comprehensive view of market momentum and potential trend shifts by combining multiple moving averages, a streak-based trend analysis system, and adaptive color visualization. It helps traders identify strong trends, spot potential reversals, and make more informed trading decisions.

Purpose

The primary goal of this indicator is to assist traders in distinguishing between sustained market movements and short-lived fluctuations. By evaluating how price behaves relative to its moving averages, and by measuring consecutive streaks above or below these averages, the indicator highlights areas where trends are likely to continue or lose momentum.

Overview

Uptrick: Time Based Reversion calculates one or more moving averages of price data and then tracks the number of consecutive bars (streaks) above or below these averages. This streak-based detection provides insight into whether a trend is gaining strength or nearing a potential reversal point. The indicator offers:

• Multiple moving average types (SMA, EMA, WMA)

• Optional second and third moving average layers for additional smoothing of first moving average

• A streak detection system to quantify trend intensity

• A dynamic color scheme that changes with streak strength

• Optional buy and sell signals for potential trade entries and exits

• A ribbon mode that applies moving averages to Open, High, Low, and Close prices for a more detailed visualization of overall trend alignment

Originality and Uniqueness

Unlike traditional moving average indicators, Uptrick: Time Based Reversion incorporates a streak measurement system to detect trend strength. This approach helps clarify whether a price movement is merely a quick fluctuation or part of a longer-lasting trend. Additionally, the optional ribbon mode extends this logic to Open, High, Low, and Close prices, creating a layered and intuitive visualization that shows complete trend alignment.

Inputs and Features

1. Enable Ribbon Mode

This input lets you activate or deactivate the ribbon display of multiple moving averages. When enabled, the script plots moving averages for the Open, High, Low, and Close prices and uses color fills to show whether these four data points are collectively above or below their respective moving averages.

2. Color Scheme Selection

Users can choose from several predefined color schemes, such as Default, Emerald, Crimson, Sapphire, Gold, Purple, Teal, Orange, Gray, Lime, or Aqua. Each scheme assigns distinct bullish, bearish and neutral colors..

3. Show Buy/Sell Signals

The indicator can display buy or sell signals based on its streak analysis logic. These signals appear as markers on the chart, indicating a “Safe Uptrend” (buy) or “Safe Downtrend” (sell).

4. Moving Average Types and Lengths

• First MA Type and Length: Choose SMA, EMA, or WMA along with a customizable period.

• Second and Third MA Types and Lengths: You can optionally stack additional moving averages for further smoothing, each with its own customizable type and period.

5. Streak Threshold Multiplier

This numeric input determines how strong a streak must be before the script considers it a “safe” trend. A higher multiplier requires a longer or more intense streak for a buy or sell signal.

6. Dynamic Transparency Calculation

The color intensity adapts to the streak’s strength. Longer streaks increase the transparency of the opposing color, making the current dominant color stand out. This feature ensures that a vigorous uptrend or downtrend is visually distinct from short-lived or weaker moves.

7. Ribbon Moving Averages

In ribbon mode, the script calculates moving averages for the Open, High, Low, and Close prices. Each of these is optionally smoothed again if the second and/or third moving average layers are active. The final result is a ribbon of moving averages that helps confirm whether the market is uniformly aligned above or below these key reference points.

Calculation Methodology

1. Initial Moving Average

The script calculates the first moving average (SMA, EMA, or WMA) of the closing price over a user-defined period.

2. Optional Secondary and Tertiary Averages

If selected, the script then applies a second and/or third smoothing step. Each of these steps can be a different type of moving average (SMA, EMA, or WMA) with its own period length.

3. Streak Detection

The indicator counts consecutive bars above or below the smoothed moving average. A running total (streakUp or streakDown) increments with every bar that remains above or below that average.

4. Reversion Intensity

The script compares the current streak value to its own average (calculated over the final chosen period). This ratio determines whether the streak is nearing a likely reversion or is strong enough to continue.

5. Color Assignment and Signals

The indicator calculates color transparency based on streak intensity. Buy and sell signals appear when the streak meets or exceeds the threshold multiplier, indicating a safe uptrend or downtrend.

Color Schemes and Visualization

This indicator offers multiple predefined color sets. Each scheme specifies a unique bullish color, bearish color and neutral color. The script automatically varies transparency to highlight strong trends and fade weaker ones, making it visually clear when a trend is intensifying or losing momentum.

Smoothing Techniques

By allowing up to three layers of moving average smoothing, the indicator accommodates different trading styles. A single layer provides faster reactions to market changes, while more layers reduce noise at the cost of slower responsiveness. Traders can choose the right balance between responsiveness and stability for their strategy, whether it is short-term scalping or long-term trend following.

Why It Combines Specific Smoothing Techniques

The Uptrick: Time Based Reversion indicator strategically combines specific smoothing techniques—SMA, EMA, and WMA—to leverage their complementary strengths. The SMA provides stable and consistent trend identification by equally weighting all data points, while the EMA emphasizes recent price movements, allowing quicker responses to market changes. WMA enhances sensitivity to recent price shifts, which helps in detecting subtle momentum changes early. By integrating these methods in layers, the indicator effectively balances responsiveness with stability, helping traders clearly identify genuine trend changes while filtering out short-term noise and false signals.

Ribbon Mode

If Open, High, Low, and Close prices remain above or below their respective moving averages consistently, the script colors the bars fully bullish or bearish. When the data points are mixed, a neutral color is applied. This mode provides a thorough perspective on whether the entire price range is aligned in one direction or showing conflicting signals.

Summary

Uptrick: Time Based Reversion combines multiple moving averages, streak detection, and dynamic color adjustments to help traders identify significant trends and potential reversal areas. Its flexibility allows it to be used either in a simpler form, with one moving average and streak analysis, or in a more advanced configuration with ribbon mode that charts multiple smoothed averages for a deeper understanding of price alignment. By adapting color intensities based on streak strength and providing optional buy/sell signals, this indicator delivers a clear and flexible tool suited to various trading strategies.

Disclaimer

This indicator is designed as an analysis aid and does not guarantee profitable trades. Past performance does not indicate future success, and market conditions can change unexpectedly. Users are advised to employ proper risk management and thoroughly evaluate trades before taking positions. Use this indicator as part of a broader strategy, not as a sole decision-making tool.

IBS (Internal Bar Strength) Trading Strategy for SPY and NDQImplementation by AlgoTradeKit

Overview

The IBS Trading Strategy is a daily bars long-only trading system, based on the concept of Internal Bar Strength (IBS). The strategy aims to identify potential reversals by monitoring how the previous bar’s close positions itself within its high-low range. It is suitable for stock and US indices. The default parameters are optimized for SPY/SPX and NDQ/QQQ

Strategy Concept

The Internal Bar Strength (IBS) is calculated using the formula:

IBS = (Previous Close - Previous Low) / (Previous High - Previous Low)

This value always lies between 0 and 1. An IBS value below 0.2 is typically interpreted as an oversold condition, while a value above 0.9 suggests an overbought state.

Trading Rules

- Long Entry :

- Condition 1 : IBS is below the user-defined entry threshold (default is 0.2).

- Condition 2 : The current price is above an N-period Exponential Moving Average (EMA) (default period is 252).

- Note : You can disable the EMA condition by setting the EMA period to 0.

- Long Exit

- The position is closed when IBS rises above the user-defined exit threshold (default is 0.9).

Customization Options

- IBS Entry Threshold : Adjust to set the sensitivity for entering a long trade based on oversold conditions.

- IBS Exit Threshold : Customize to define the exit point when the market becomes overbought.

- EMA Period : Set the lookback period for the EMA to align with your trend bias; disable this condition by setting the period to 0.

Risk Management & Trading Considerations

- Designed for daily charts, the strategy captures higher timeframe trends and minimizes noise.

- The entry and exit conditions are straightforward, aiming to avoid over-trading while letting clear signals dictate trade management.

- Always use proper risk management techniques and test the strategy thoroughly on historical data and in a simulated environment before applying it in live markets.

Disclaimer

This strategy is for educational and informational purposes only and does not constitute financial advice. Trading involves risk, and past performance is not indicative of future results. Always conduct your own research and consider your risk tolerance before making any trades.

3 Red / 3 Green Strategy with Volatility CheckStrategy Name: 3 Red / 3 Green Strategy with Volatility Check by AlgoTradeKit

Overview

This long-only strategy is designed for daily bars on NASDAQ (or similar instruments) and combines simple price action with a volatility filter. It “tells it like it is” – enter when the market shows weakness, but only in sufficiently volatile conditions, and exit either on signs of a reversal or after a set number of days.

Entry Conditions

- Price Action :

Enter a long position when there are 3 consecutive red days (each day's close is below its open).

- Volatility Filter :

The entry is allowed only if the current ATR (Average True Range) calculated over the specified ATR Period (default 12) is greater than its 30-day simple moving average. This ensures the market has enough volatility to justify the trade.

Exit Conditions

- Reversal Signal :

Exit the long position when 3 consecutive green days occur (each day's close is above its open), signaling a potential reversal.

- Time Limit :

Regardless of market conditions, any open trade is closed if it reaches the Maximum Trade Duration (default 22 days). This helps limit exposure during stagnant or unfavorable market conditions.

- You can toggle the three-green-day exit if you want to isolate the time-based exit.

Input Parameters

- Maximum Trade Duration (days): Default is 22 days.

- ATR Period: Default is 12.

- Use 3 Green Days Exit: Toggle to enable or disable the three-green-day exit condition.

How It Works

1. Entry: The strategy monitors daily price action for 3 consecutive down days. When this occurs and if the market is volatile enough (current ATR > 30-day ATR average), it opens a long position.

2. Exit: The position is closed if the price action reverses with 3 consecutive up days or if the trade has been open for the maximum allowed duration - i.e. use it on daily chart.

Risk Management

- The built-in maximum trade duration prevents trades from lingering too long in a non-trending or consolidating market.

- The volatility filter helps ensure that trades are only taken when there is sufficient price movement, potentially increasing the odds of a meaningful move.

Disclaimer

This strategy is provided “as is” without any warranties. It is essential to backtest and validate the performance on your specific instrument and market conditions before deploying live capital. Trading involves significant risk, and you should adjust parameters to match your risk tolerance.

Test and tweak this strategy to see if it fits your trading style and market conditions. Happy trading!

Liquidity Sweep Filter [AlgoAlpha]Unlock a deeper understanding of market liquidity with the Liquidity Sweep Filter by AlgoAlpha. This indicator identifies liquidity sweeps, highlighting key price levels where large liquidations have occurred. By visualizing major and minor liquidation events, traders can better anticipate potential reversals and market structure shifts, making this an essential tool for those trading in volatile conditions.

Key Features :

🔍 Liquidity Sweep Detection – Identifies and highlights areas where liquidity has been swept, distinguishing between major and minor liquidation events.

📊 Volume Profile Integration – Displays a volume profile overlay, helping traders spot high-activity price zones where the market is likely to react.